Macro Challenges: A Confluence of Economic Uncertainty

As the world braces itself for an impending recession, the question is not whether it will occur, but how extensive and prolonged it will be. Recent indicators suggest that the economic outlook is rapidly deteriorating across three major economic regions: the US, China, and the eurozone.

Deteriorating Economic Outlook

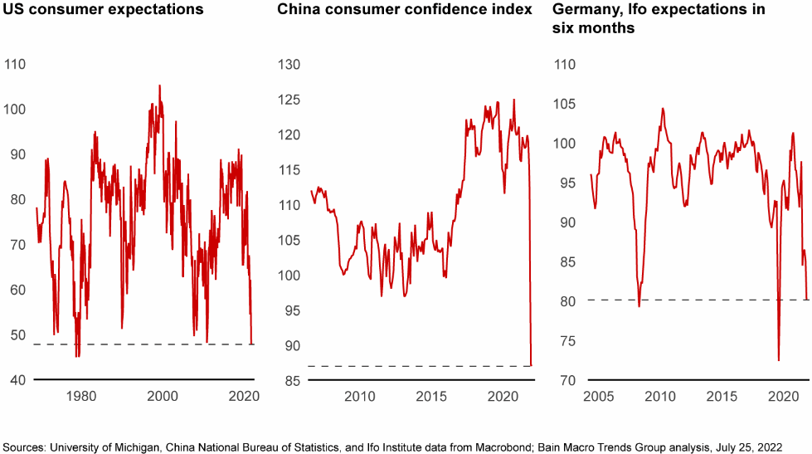

Recent surveys show that the economic outlook is deteriorating at an alarming rate in three major economic regions. In the US, consumer expectations have plummeted to levels not seen since 1980. Similarly, Chinese consumer confidence has taken a nosedive, primarily due to lockdowns and a struggling property sector. Finally, expectations in the eurozone, as gauged by a key German business survey, have declined to levels reminiscent of the global financial crisis (Figure 1).

The Global Credit Cycle

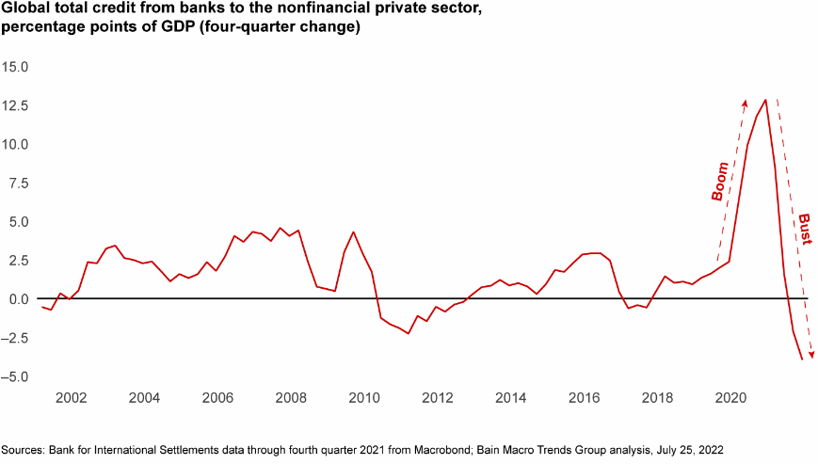

The dramatic fall in the macroeconomic outlook can be attributed to the large boom-to-bust trajectory of global credit. Lending increased by 14 percentage points (relative to world output) between the fourth quarter of 2019 and the first quarter of 2021, peaking at 119% of gross world product. However, global lending has since declined by 5 percentage points in just three quarters (data available through the end of 2021). In contrast, the Federal Reserve has only recently begun to tighten monetary policy, and the European Central Bank raised rates in July for the first time in 11 years (from negative 0.5% to 0%). In comparison, liquidity fell only 4 percentage points after the global financial crisis, despite expansive interventions from the Fed and ECB that were considered unprecedented at the time (Figure 2).

Regional Economic Stresses

Each of the three major economic regions is facing unique challenges. In the US, inflation is the predominant issue, with rising home mortgage lending rates driving inflation-adjusted new mortgage costs beyond their 2006 peaks. In China, the property sector is grappling with mortgage boycotts and bailout programs, while recent lockdowns have resulted in the country's second quarterly GDP contraction in modern economic history. In Western Europe, energy prices and rationing are threatening the region's industrial base and broader economy, with the eurozone's producer price index surging 42% since January 2021. Notably, key benchmark natural gas prices were already on the rise before the outbreak of war in Ukraine, suggesting that energy supply challenges may persist even after the war's conclusion.

Global Convergence of Challenges

Although each region has its own set of challenges, these issues are converging and may culminate in a globally synchronized downturn in the second half of 2022 and into 2023, just two years after the last one. The focus for businesses has shifted from questioning the likelihood of a recession to assessing its potential breadth and depth. The role of major central banks and their ability to use financial system inflation to mitigate downturns will be a key factor. The swift liquidity support provided by central banks during the 2008–2009 financial crisis and the early months of the pandemic was crucial for crisis management and recovery. However, inflation was not a complicating factor during those crises, as it is today. Therefore, the critical question for the global economy is whether this time will be different.

Talk to Us